Environmental penalties and commodity market dynamics: Empirical evidence from Chinese listed companies and associated futures price volatility

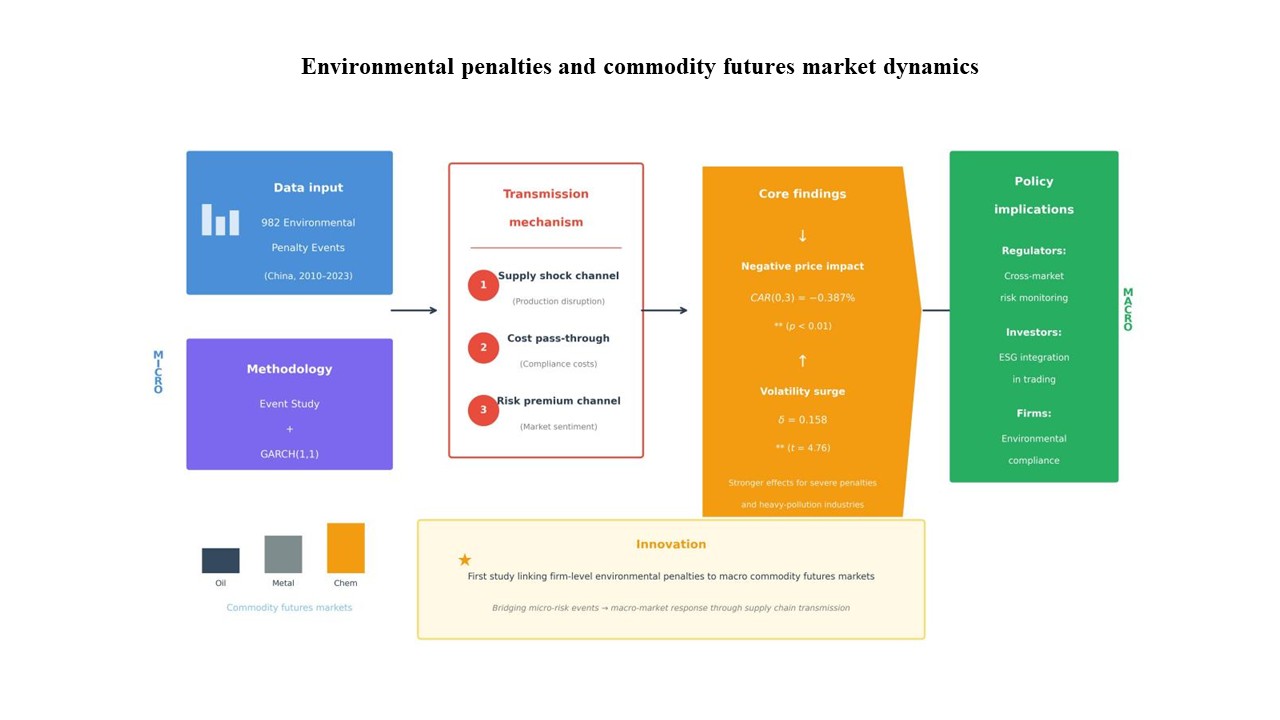

As ecological civilization and dual carbon goals advance, environmental risk has emerged as a crucial factor influencing corporate performance and financial market stability. This study examines whether and how firm-level environmental penalty events transmit into commodity futures markets, identifying the underlying transmission mechanisms and moderating factors. We manually collect a comprehensive dataset of 982 environmental penalty announcements issued to Chinese A-share listed companies from 2010 to 2023, matching these with price data from the most directly linked commodity futures (e.g., industrial metals and agricultural products). The results show that environmental penalties significantly induce negative price reactions and elevate volatility in corresponding commodity futures markets. This effect is particularly pronounced for penalties in pollution-intensive industries. Within 1–3 trading days following a penalty announcement, cumulative abnormal returns of related futures contracts are significantly negative (p<0.01). Generalized autoregressive conditional heteroskedasticity model estimates confirm a notable increase in conditional volatility on the announcement day, accompanied by stronger risk-averse sentiment in the market. This study elucidates the micro-transmission mechanism of corporate environmental risk to commodity markets, offering investors a fresh lens for risk pricing and providing empirical support for regulators in constructing environmental risk monitoring systems. The findings carry important policy implications: (1) Commodity futures markets serve as an effective channel for pricing environmental risk; (2) regulators should consider cross-market spillover effects when designing environmental penalty disclosure policies; and (3) commodity market participants should incorporate environmental risk assessments into their trading strategies. These insights support enhancing financial markets’ role in the green transition.

- Tian Y, Song S, Ma J. Digital transformation on corporate environmental performance. Front Bus Econ Manag. 2024;16(3):175-182. doi: 10.54097/vv8n8304

- Su D, Lian L. Does green credit affect the investment and financing behavior of heavily polluting enterprises? J Financ Res. 2018;12:123-137. In Chinese.

- Lo CKY, Tang CS, Zhou Y, Yeung ACL, Fan D. Environmental incidents and the market value of firms: An empirical investigation in the Chinese context. Manuf Serv Oper Manag. 2018;20(3):422-439. doi: 10.1287/msom.2017.0680

- Ahmed AD, Huo R. Volatility transmissions across international oil market, commodity futures and stock markets: Empirical evidence from China. Energy Econ. 2021;93:104741. doi: 10.1016/j.eneco.2020.104741

- Kang SH, McIver R, Yoon SM. Dynamic spillover effects among crude oil, precious metal, and agricultural commodity futures markets. Energy Econ. 2017;62:19-32. doi: 10.1016/j.eneco.2016.12.011

- Li S, Zhang Y. Environmental risk and stock price crash risk: Evidence from energy substitution policy adoption. Int Rev Econ Finance. 2025;99:103977. doi: 10.1016/j.iref.2025.103977

- Zhang X, Ma Z. ESG and the high-quality development of China’s listed companies under the dual carbon goal: An empirical analysis based on ESG “101” framework. J Beijing Univ Technol Soc Sci Ed. 2022;22(5):101-122. doi: 10.12120/bjutskxb202205101

- Wang Y, Wang WW. The impact of environmental disasters on bank default rates: A theoretical and empirical analysis. J Finance Res. 2021;(12):38-56. In Chinese.

- Fourné M, Li X. Climate policy and international capital reallocation. J Financ Stab. 2025;76:101495. doi: 10.1016/j.jfs.2025.101495

- Ahmed WMA. How do green vis-à-vis brown energy stock markets respond to climate risks? Financ Res Open. 2025;1(4):100066. doi: 10.1016/j.finr.2025.100066

- Cai Y, Cui J. A study on the climate vulnerability of Chinese commercial banks under the impact of climate transition risks: An empirical analysis based on a stress test model. Wuhan Finance. 2023;10:3-12.

- Herbst AF, Marshall JF, Wingender J. An analysis of the stock market’s response to the Exxon Valdez disaster. Glob Finance J. 1996;7(1):101-114. doi: 10.1016/S1044-0283(96)90016-2

- Cheng B, Ioannou I, Serafeim G. Corporate social responsibility and access to finance. Strateg Manage J. 2014;35(1):1-23. doi: 10.1002/smj.2131

- Friede G, Busch T, Bassen A. ESG and financial performance: Aggregated evidence from more than 2000 empirical studies. J Sustain Finance Invest. 2015;5(4):210-233. doi: 10.1080/20430795.2015.1118917

- Capelle-Blancard G, Petit A. Every little helps? ESG news and stock market reaction. J Bus Ethics. 2019;157:543-565. doi: 10.1007/s10551-017-3667-3

- Serafeim G, Yoon A. Which corporate ESG news does the market react to? Financ Anal J. 2022;78(1):59-78. doi: 10.1080/0015198X.2021.1973879

- Avramov D, Cheng S, Lioui A, Tarelli A. Sustainable investing with ESG rating uncertainty. J Financ Econ. 2022;145(2):642-664. doi: 10.1016/j.jfineco.2021.09.009

- Pástor Ľ, Stambaugh RF, Taylor LA. Sustainable investing in equilibrium. J Financ Econ. 2021;142(2):550-571. doi: 10.1016/j.jfineco.2020.12.011

- Shen H, You J, Liu J. Do environmental inspections improve the cost of equity capital? Evidence from Chinese listed companies. J Financ Res. 2010;12: 159-172. In Chinese.

- Krueger P, Sautner Z, Starks LT. The importance of climate risks for institutional investors. Rev Financ Stud. 2020;33(3):1067-1111. doi: 10.1093/rfs/hhz137

- Bolton P, Kacperczyk M. Do investors care about carbon risk? J Finance Econ. 2021;142(2):517-549. doi: 10.1016/j.jfineco.2021.05.008

- Wu N, Xiao W, Liu W, Zhang Z. Corporate climate risk and stock market reaction to performance briefings in China. Environ Sci Pollut Res. 2022;29(36):53801-53820. doi: 10.1007/s11356-022-19479-2

- Birindelli G, Miazza A, Paimanova V, Palea V. Just “blah blah blah”? Stock market expectations and reactions to COP26. Int Rev Financ Anal. 2023;88:102699. doi: 10.1016/j.irfa.2023.102699

- Drake S, Lundberg J, Lundberg S. Market response to environmental policy via public procurement: An empirical analysis of bids and prices. J Environ Manage. 2024;365:121547. doi: 10.1016/j.jenvman.2024.121547

- Shen H, Huang N. Can carbon emissions trading mechanism improve firm value? Finance Trade Econ. 2019;40(1):144-161. In Chinese.

- Sun C, Chen Z, Sun B. The externalities and industrial green transformation effects of carbon trading system. Econ Res J. 2025;60(6):134-151. In Chinese.

- Niu HW, Cao LL. Carbon prices, green investment and corporate credit risks. China Ind Econ. 2024;(8): 118-136. In Chinese.

- Han J, Liu RX, Yue W. Global green trade, environmental rule governance and China’s path choice. China Ind Econ. 2024;(1):17-35. In Chinese.

- Dai X, Ma HW. Heterogeneity of FTA environmental protection clauses, internal-external differentiation and export green transformation. China Ind Econ. 2024;(4):95-113. In Chinese.

- Zhang BB, Yu L, Cai HB. Carbon tariff shocks and the “buffer valve” effect of expanding and pricing China’s carbon market. China Ind Econ. 2025;9:5-21. In Chinese.

- Niu M, Wang ZG, Zhang YB. From territorial to ownership-based: How global value chain restructuring affects the implicit economic-environmental effects of China’s trade. China Ind Econ. 2025;9:99-116. In Chinese.

- Xu M. How local government environmental concerns drive enterprises’ green and low-carbon transformation: Empirical evidence based on text analysis. J Jiangxi Univ Sci Technol. 2024;45(4):72-84. In Chinese. doi: 10.13265/j.cnki.jxlgdxxb.2024.04.010

- Li Q, Xiao Z. Environmental regulation, green technological innovation, and industrial green development. Econ Res J. 2020;55(9):192-208. In Chinese.

- Li QY, Xiao ZH. Heterogeneous environmental regulation tools and corporate green innovation incentives— evidence from green patents of listed companies. Nankai Econ Stud. 2022;4:120-138. In Chinese.

- Tan Z, Zhang Y, Liu C, et al. Investors’ extrapolative expectations and anomalies in the China’s stock market. Econ Res J. 2024;59(2):97-115. In Chinese.

- Brown SJ, Warner JB. Using daily stock returns: The case of event studies. J Finance Econ. 1985;14(1): 3-31. doi: 10.1016/0304-405X(85)90042-X

- MacKinlay AC. Event studies in economics and finance. J Econ Lit. 1997;35(1):13-39.

- Bollerslev T. Generalized autoregressive conditional heteroskedasticity. J Econ. 1986;31(3):307-327. doi: 10.1016/0304-4076(86)90063-1

- Wang YD, Wu CHF. Forecasting energy market volatility using GARCH models: Can multivariate models beat univariate models? Energy Econ. 2012;34(6):2167-2181. doi: 10.1016/j.eneco.2012.07.010

- Yang K, Tian F, Chen L, Li S. Realized volatility forecast of agricultural futures using the HAR models with bagging and combination approaches. Int Rev Econ Finance. 2017;49:276-291. doi: 10.1016/j.iref.2017.01.030